If you’ve ever wondered when is the right time to make an estate plan, the answer is simple: now. It’s never too early to take charge of your financial affairs or life plan. But there are some key moments in life when creating or updating your estate plan becomes especially important.

As life evolves, so should your estate plan. From major life milestones to unexpected changes, your estate plan should reflect your stage of life and the people you care about most. That’s where Herbie comes in––guiding you through crafting and revising your plan at every stage of life. Let’s explore our Top Ten of these pivotal times:

1. Marriage – New Partner, New Plan

Marriage brings with it new financial and legal considerations. For example, you may now have jointly-owned assets. You also will have joint plans and goals. Updating your estate plan will ensure that your spouse is adequately provided for and reflects your joint wishes.

- Pro tip: Don’t forget to review and update your beneficiary designations on bank, brokerage and retirement accounts, as well as any life insurance policies that you have.

2. Birth of a Child – Protecting Your Legacy

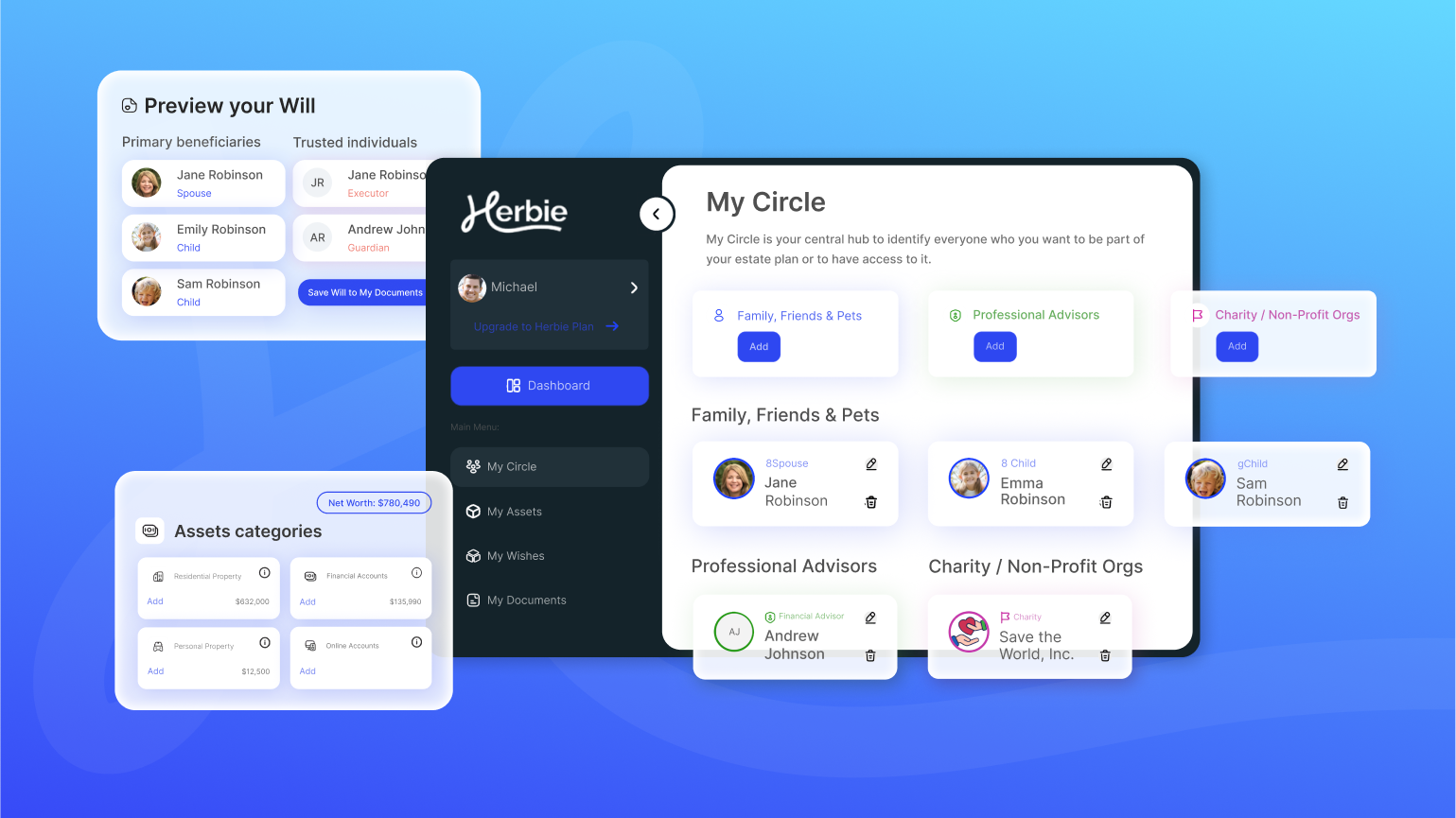

As your family grows with the birth of a child, so should your estate plan. It’s the right time to review your prior wishes to see how they have now changed. If you haven’t yet made a Will, it’s the perfect time. Also, you should think about a Guardian who could help raise your children in case something happens to you.

- Longterm Care for Kids: In case something happens to you (and your spouse), someone will have to be appointed to take care of your minor children. In your Will, you can name a Guardian to care for your children if something happens. Think about who you view as a responsible person and where you’d want your kids to grow up. Most people name parents, a sibling or another close family member or friend.

- Double Check: Make sure you continue to review and update your beneficiary designations as you have additional children so that they account for all your kids and not just the firstborn.

3. Buying a Home – Big Investments

For many, a home is their most significant asset.

- Understand Joint Succession: It’s common to buy a home as Joint Tenants with your spouse. Know that if something is owned as joint tenants (technically, joint tenants with rights of survivorship, or JTWROS), the home will automatically pass to the surviving spouse, unrelated to whatever your Will says.

- Reflect: When you buy your home, take a pause, reflect and reassess your financial situation and overall goals.

4. Divorce – Fresh Start, Fresh Plan

Like marriage, divorce is a turning point in life, including for your estate plan.

- Review, Revise, Excise: It’s likely true that after your divorce, you won’t want to keep your ex-spouse in your estate plan the way he or she was in it before. Make sure (assuming it’s your wish) to remove your ex-spouse as a beneficiary under your Will, bank and brokerage accounts and life insurance policies.

- New Trusted Individuals: You’ll also want to update your trusted individuals, including who is to serve as Executor under your Will, Trustee under your Trust, and your legal representative under a Power of Attorney or Healthcare Directive if you’re incapacitated.

5. Falling Out – New Friends In

Relationships change, and so should your plan. Friends and professional advisors mostly come up in estate plans serving in trusted roles: for example, as your Executor or Trustee administering your estate after you pass away, or as Guardian, taking care of your kids if something happened to you. They also may be a beneficiary under your estate plan.

- Keep Trusted Individuals Current: It’s important to review who you want to serve in these important estate roles from time to time. As relationships change, so too should these trusted appointments.

- No Mistaken Gifts: Some people leave gifts of cash or an item to a friend in their Will. If the friendship ends, make sure you review that bequest too.

6. Death of a Loved One – Seeing the Effects

The loss of a loved one highlights the importance of estate planning.

- The Good and the Bad: You may realize that a loved one had a good estate plan, or had no estate plan at all. Learn from the good and the bad that you see from others’ plans, or the lack thereof.

- Review Your Heirs: Review the people who you want to be the heirs of your estate and how they could be best provided for. You also may inherit from a loved one after they pass away, which could potentially impact the way you plan for your family.

7. Children Getting Married (or Divorced) – Expanding and Contracting Families

When your child gets married, all of a sudden you’ll have to think of a new person: your son-in-law or daughter-in-law.

- Joining Assets Together: It’s common for a young married couple to join together much or all of their assets into joint accounts. Similarly, when a spouse receives an inheritance after the passing of a loved one, it’s common for that money to be deposited into a joint account. So you will have to take the spouse into account. For example, the spouse will play a role in how the money will be spent. But a bigger concern arises if your child gets divorced, as the assets you set aside for your child may end up in the hands of the ex in divorce proceedings.

8. Grandchildren – Expanding the Family

If you have grandchildren, it’s time to rethink whether your estate plan includes and protects your growing family going forward.

- Direct Support: Some grandparents specifically include a provision for grandchildren in their Will or trust, although most assume that their children will take care of their grandkids with the funds they receive. But remember: if you provide for one grandkid, then when more are born, be sure to go back and update for the new grandkids.

- Education and Healthcare: Direct payments to educational institutions and healthcare providers are generally excluded from the federal gift tax (to be addressed in a future article).

9. Retirement – Planning for the Golden Years

We hope you relax when you retire, but it’s also a pivotal time to re-evaluate your estate plan, not only in terms of after you pass, but also in case you become incapacitated.

- New Trustworthy People: Ensure that the people you formerly named to be your Executors and Trustees, or your representatives in the event of incapacity, are still the right choice. As those people age, consider whether you should update your plan with younger individuals.

- Plan for Incapacity: Make sure to have in place a Power of Attorney to appoint someone to take care of finances if you’re not able to, and an Advance Healthcare Directive or Healthcare Proxy (the name of the document changes in different states) to take care of your healthcare decisions if you are incapacitated. With Herbie, you’ll be able to make, view and revise these documents.

10. Old Age – Peace and Security

Whether for yourself or an aging loved one, when a person is in their final years, this is the time to make sure all is in order.

- Tally Assets: Make sure someone knows the universe of the elderly individual’s financial plan as best as he or she is allowed or able to learn (some elderly individuals are more inclined to share than others).

- Who Will Administer the Estate?: With Herbie, you can designate your trusted individuals (like Executors and Trustees) to have access right as a loved one passes away, to be immediately ready to step in. With Herbie, you can designate these individuals and empower them with our Admin Co-Pilot to tackle the steps involved in administering an estate.

Your Plan with Herbie

Life doesn’t stand still, and neither should your estate plan.

With Herbie, you’re never alone in your life journey through estate planning. No matter what stage you’re at, we’re here to clarify the estate planning process and help transition you and your family towards estate administration.

Join our waitlist today in advance of our Spring launch.