Join the waitlist to secure early pricing.

Most people know they need a will. Far fewerMost people know they need a will. Only 24% of Americans actually have one, and the reason usually comes down to not knowing where to start.

A will preparation checklist breaks the process into clear steps: inventorying assets, choosing an executor, naming beneficiaries and guardians, gathering documents, and understanding how to sign and store everything properly. This guide walks through each step so you can move from "I should do this" to "done."

A last will and testament is a legal document that names who receives your assets, appoints an executor to settle your estate, and designates guardians for minor children. Without one, your state's intestacy laws make all of those decisions for you, and the results rarely match what you'd actually want.

A will puts you in control. You decide who inherits your home, your savings, and your grandmother's ring. You pick the person who raises your kids if something happens. And you choose who handles the paperwork and logistics after you're gone.

Follow this sequence, and you'll have everything ready to create a legally valid will.

Start by listing everything you own and everything you owe. This financial snapshot becomes the foundation of your entire estate plan.

You don't need exact values for everything right now. Ballpark figures work fine at this stage because the goal is a complete picture, not a perfect one.

Digital assets are easy to overlook, yet they often hold real value. Cryptocurrency, online banking credentials, social media accounts, cloud-stored photos, and subscription services all count as digital assets.

One important note: don't list passwords directly in your will. Wills become public record during probate, so anyone could see them. Instead, document digital assets separately in a secure password manager or encrypted file, then tell your executor where to find it.

Having the right paperwork on hand speeds up the entire process.

| Document Type | Examples |

|---|---|

| Personal identification | Birth certificate, Social Security card, passport |

| Marriage/divorce records | Marriage license, divorce decree, prenuptial agreement |

| Financial records | Bank statements, investment accounts, recent tax returns |

| Property documents | Real estate deeds, vehicle titles, mortgage statements |

| Insurance policies | Life insurance, homeowner's, auto with policy numbers |

| Debt documentation | Loan agreements, credit card statements |

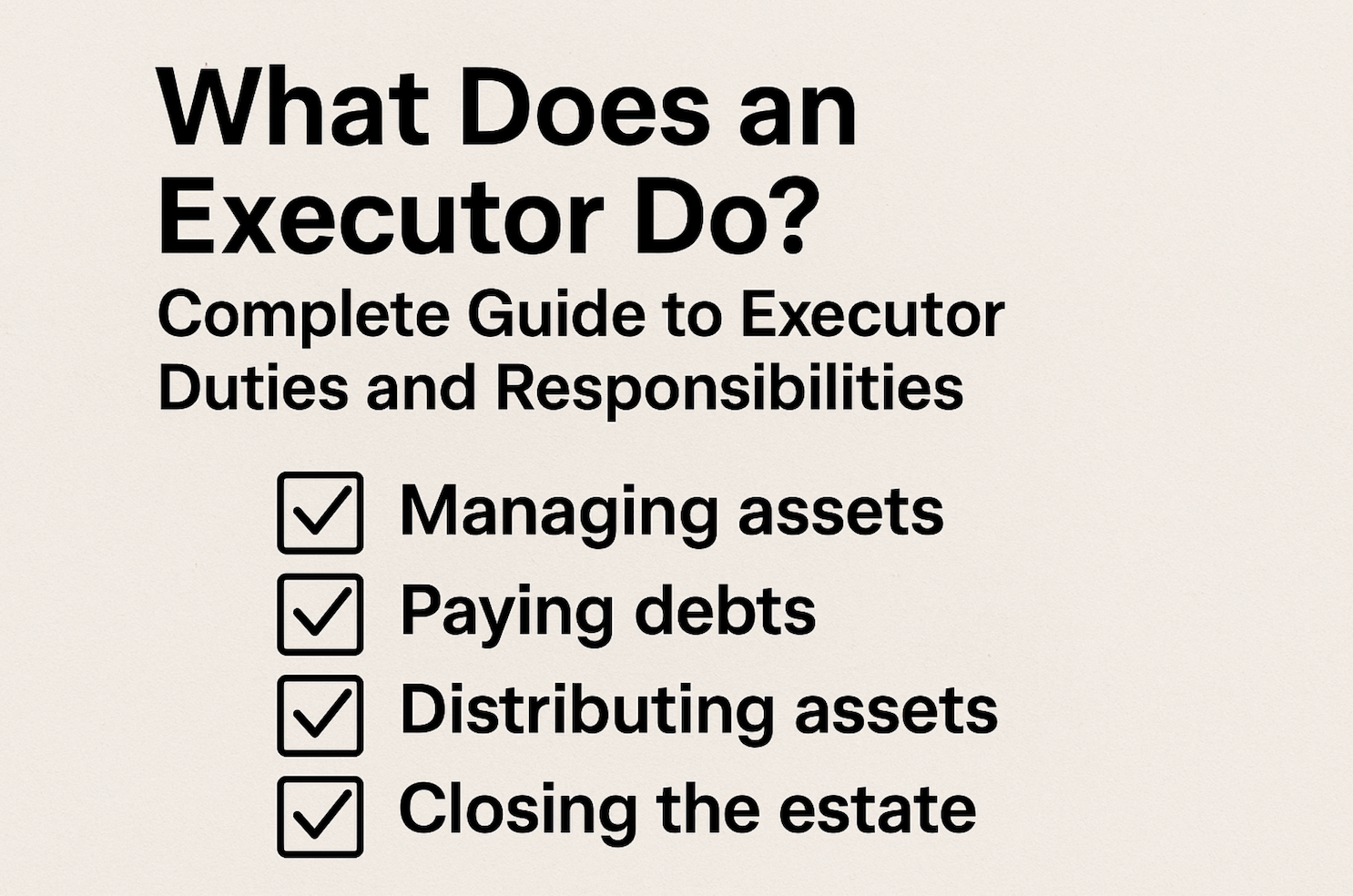

Your executor is the person who handles everything after you're gone. This includes paying debts, filing paperwork, and distributing assets to beneficiaries. The role requires organization, patience, and trustworthiness.

Most people choose a spouse, adult child, or close friend. Whoever you pick, have a conversation with them first to make sure they're willing. And always name a backup executor in case your first choice can't serve when the time comes.

Beneficiaries are the people or organizations who receive your assets. You can name family members, friends, or charities.

Be specific with names. "My children" works, but "my daughter Sarah Chen and my son Michael Chen, in equal shares" is clearer and less likely to cause confusion. Also include a disaster clause, which specifies what happens if a beneficiary dies before you. Without one, that share might not go where you'd expect.

For parents, this is often the most important decision in the entire will. A guardian is the person who raises your children if both parents die.

Think carefully about values, parenting style, and practical factors like location. Talk to potential guardians before naming them because it's a significant responsibility. And name alternates, since circumstances change over time.

Funeral preferences, burial versus cremation, memorial service instructions: none of this is legally binding, but it guides your family during a difficult time.

Keep this section brief. Detailed funeral planning belongs in a separate document, not your will.

Having everything ready makes the process dramatically faster. Here's what to gather.

Current statements show account numbers and approximate values. You'll reference this information when describing what you're leaving to whom.

Deeds and titles prove ownership. Your executor will need them to transfer assets after your death.

Here's something many people miss: life insurance and retirement accounts typically pass by beneficiary designation, not through your will. Document the policy numbers and current beneficiaries so everything stays coordinated.

Create a secure list of your online accounts, including email, social media, financial services, and subscriptions. A password manager works well for this purpose. Your executor will thank you later.

Birth certificates, Social Security cards, and passports confirm identity and may be required during estate settlement.

A will is one piece of a complete estate plan. Several related documents work alongside it.

A revocable living trust holds assets during your lifetime and transfers them after death, often without going through probate. Probate, which typically costs 3–8% of an estate's value. Probate is the court process that validates a will and oversees asset distribution. A trust is optional but worth considering for larger estates or if privacy matters to you.

A trust works with your will, not instead of it. Herbie helps you create both in one platform.

A financial power of attorney authorizes someone to manage your finances if you become incapacitated. It covers situations while you're alive but unable to act, which is completely different from what a will does.

An advance healthcare directive provides instructions for medical care if you can't communicate. Despite the similar name, a "living will" is about medical decisions, not asset distribution.

Retirement accounts, life insurance, and some bank accounts pass directly to named beneficiaries regardless of what your will says. Review beneficiary designation forms alongside your will to avoid conflicts between the two.

Proper execution is critical. An improperly signed will can be completely invalid.

Most states require two witnesses who watch you sign. Witnesses generally cannot be beneficiaries named in the will. Some states have additional requirements, like age minimums for witnesses.

Some states require notarization while others make it optional but recommended. A self-proving affidavit, which is a notarized statement from you and your witnesses, can significantly speed up probate later.

Herbie provides state-specific signing instructions so you know exactly what your state requires.

A will that can't be found is as bad as no will at all.

Digital copies serve as useful backups, though the signed original is what matters legally. Herbie offers secure cloud-based document storage with encryption.

Tell your executor where to find the originalTell your executor where to find the original — only 46% of executors were even aware a will existed. Consider sharing access with trusted family members or your financial advisor. Surprises during grief rarely go well.

A will isn't one-and-done. Life changes, and your will can keep up.

Marriage may automatically revoke a previous will in some states. Divorce typically removes an ex-spouse as a beneficiary, but laws vary by state.

New children can be added as beneficiaries, and guardian nominations may require updating.

Buying or selling property, receiving an inheritance, or significant changes in net worth are all good reasons to review your will.

Estate laws vary by state. A will valid in California may require adjustments when you move to Texas.

If someone named in your will dies, update it with new appointments or alternate beneficiaries.

A few common errors invalidate wills or cause family conflict. Here's how to sidestep them.

Retirement accounts and insurance pass by beneficiary form, not your will. Outdated beneficiaries on retirement accounts and insurance policies override whatever your will says.

Improper execution is the most common reason wills get contested. Follow your state's requirements exactly.

Cryptocurrency, online accounts, and digital files have real value. Address them in your estate plan.

If your primary executor can't serve, the court appoints someone unless you've named a backup.

Discuss your wishes with family. Surprises during an emotional time often lead to conflict.

A lawyer isn't legally required in most states. For straightforward situations with no blended families, no business ownership, and a modest estate, online platforms with attorney-vetted templates work well.

Complex situations benefit from personalized legal advice. Herbie is a technology service, not a law firm, and doesn't provide legal advice. However, the platform's state-compliant templates cover most common scenarios.

Costs range widely depending on your approach:

Herbie offers high-quality estate planning documents at no cost, making the "too expensive" excuse obsolete.

Planning a will doesn't have to be complicated or expensive. Gather your documents, make decisions about your executor, beneficiaries, and guardians, create your will, sign it properly, store it safely, and update it when life changes.

Get started with Herbie's free estate planning platform to create your will in minutes.

Your state's intestacy laws decide who gets your assets, which may not match your wishes at all. The court also appoints someone to manage your estate and selects guardians for minor children.

Most states don't require notarization for a will to be valid. However, a notarized self-proving affidavit can simplify probate significantly.

Common reasons include lack of proper witnesses, the creator wasn't of sound mind, the will was created under duress, or it wasn't executed according to state law.

With documents gathered and decisions made, creating a basic will can take as little as an hour using an online platform.

Select someone trustworthy, organized, and willing to serve. The person you choose will be handling financial and legal paperwork during what's often an emotional time.